Ukraine crisis briefing

Powered by

Download GlobalData’s Ukraine Crisis Executive Briefing report

- ECONOMIC IMPACT -

Latest update: 6 May

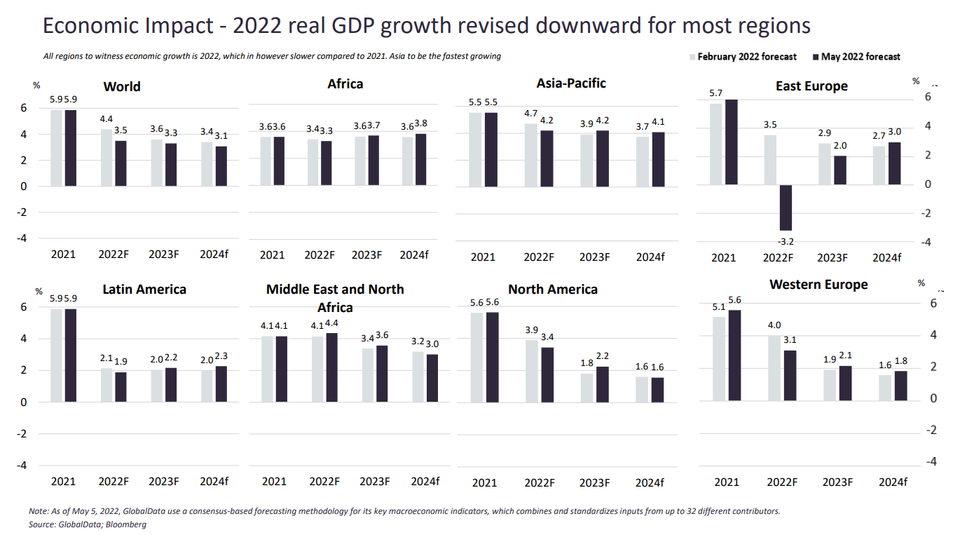

GlobalData forecasts the world economy will grow at just 3.5% in 2022 following 5.9% growth in 2021. At the same time, the global inflation rate is projected to rise to 6.5% in 2022 from 3.5% in the previous year due to supply chain disruption amid the Ukraine-Russia war.

Rising commodity prices as a result of the Ukraine conflict will strain the apparel industry throughout Europe as the impact has wider consequences on the supply chain, the price of textiles, and is contributing to further inflationary pressure on consumers’ pockets, which will result in spending being diverted away from apparel purchases to more essential items across Europe.

6%

Consensus forecast for world GDP growth in 2021

6%

Unemployment rate in OECD nations in August 2021

- SECTOR IMPACT: APPAREL -

Latest update: 6 May

Industry predictions

Sanctions

Supply chain and demand disruption

Commodity price impact

BACK TO TOP